According to Statista, the European ecommerce market is on track to reach a remarkable $888.1 billion by 2028, offering merchants a world of possibilities for global expansion.

However, diving into this market goes beyond acknowledging its size. It requires a good understanding of its characteristics, especially regarding payment methods.

Unlike the more homogenous payment landscape in the US, which relies heavily on card transactions, Europe boasts a range of payment options, each shaped by unique consumer preferences and market dynamics.

From the Nordic countries to the Mediterranean shores, diverse financial sceneries unfold across the continent.

In this article, we explore some of the most popular payment methods in Europe and touch on market dynamics.

From Cash To Cashless: A Shift in Consumer Preferences

Non-cash payments are on the rise globally, and Europe is no exception. The trend is expected to continue, with transactions estimated to go up from 286.5 billion in 2022 to 466.8 billion by 2026, according to the European Central Bank data.

As reported by the European Commission, a significant 55% of European citizens favor cashless payment, while 22% opt for cash, and 23% have no preference.

Factors such as the convenience, security, and speed of non-cash payment methods are driving this shift.

Cards Dominate in Europe, Yet Other Payment Methods Gain On Popularity

While new payment methods like instant account-to-account transfers and request-to-pay are becoming popular, debit cards remain the top choice for payments in Europe.

In fact, cards account for 57.3% share of all non-cash payments on the continent, with credit transfers and direct debit payments making up over 40% of the remaining share.

What’s interesting is that Europe keeps trying to diversify the payment industry to challenge the dominance of Visa and Mastercard.

Various initiatives have been introduced to achieve this goal, such as the European Payments Initiative (EPI), ongoing efforts to promote open banking, and a new instant payments law proposal.

Local Payment Methods Steal the Show

The payment landscape in Europe is diverse with various cashless payment methods gaining popularity in different countries.

Let’s discover the fascinating variety of payment options available as Europe moves closer to a cash-free society.

iDEAL

There’s no doubt that The Netherlands is one of the European leaders when it comes to cashless payments.

This can be attributed to the country’s efficient banking infrastructure and the popularity of iDEAL — a local online payment method directly linked to Dutch bank accounts.

Established in 2005, iDeal has emerged as the dominant online payment solution in the Netherlands, with a 70% market share.

An interesting fact is that over 50% of iDEAL payments are made outside ecommerce.

iDEAL offers a convenient online payment option where customers can securely complete transactions with their bank credentials.

When using iDEAL, customers are directed to their online banking platform, where they undergo a two-step authentication process.

Needless to say, they instantly get notified about the payment status.

Bancontact

Belgium is another example of a European country that prioritizes cashless transactions. Its domestic payment system, Bancontact, is more popular than major global card networks, as per Statista.

With over 17 million cards in circulation, Bancontact offers versatile payment options. Whether it’s online transactions, contactless payments in physical stores using a Bancontact card, or Payconiq through the Bancontact app with a QR code, customers enjoy a range of choices.

The security of online payments with Bancontact is top-notch, taking place within the customer’s Internet banking environment for maximum safety.

A significant advantage is that Bancontact payments are guaranteed and cannot be reversed, ensuring immediate confirmation for both customers and merchants.

MobilePay

According to the Danmarks Nationalbank’s survey, Denmark has been ranked as one of the most digitized European countries when it comes to payments, with MobilePay playing a significant role in this trend.

It was first introduced in 2013 as the first mobile phone-based payment solution by Danske Bank, and since then, it has grown rapidly. It is now used by all banks in Denmark and widely popular in Finland.

Customers wishing to pay with MobilePay must register their card in the app. Once done, they can enjoy a simple and convenient way to make mobile payments without the need to enter their card or account details.

Trustly

Trustly is a Swedish banking company that provides instant payment services without the need for third-party payment processors. It’s widely accepted by online merchants across Europe — in the Netherlands, Norway, Finland, Sweden, the UK, and many other countries.

To ensure the highest security standards, Trustly never stores sensitive information. Instead, it relies on advanced encryption techniques, thus protecting customers’ data from being stolen and used for fraud.

Another interesting fact is that it has been recognized as a Preferred Partner for Online Banking Payment & Verification by Nacha — a body regulating ACH transactions in the United States.

Zimpler

Without a doubt, Scandinavian countries have a lot to offer when it comes to payment solutions. Another example worth mentioning is Zimpler, which stands out for its simplicity and high level of security.

Although it was initially developed for the online gaming and betting industry, Zimpler has expanded its reach to various ecommerce sites, making it a valuable addition to the payment landscape.

Designed primarily for mobile devices, Zimpler offers a quick and convenient way to make payments on the go.

With its instant and secure open banking payments, this Swedish technology platform can help businesses streamline their transactions, save time, and build stronger customer relationships.

Paysafecard

For Europeans who prefer the convenience of a prepaid option over traditional payment methods, Paysafecard — bypassing the need for credit cards or bank accounts — comes in handy. Plus, the customers can choose between two types of Paysafecard: the classic/PIN option and the physical prepaid card by Mastercard.

With Paysafecard, users can purchase prepaid cards that can be used to make purchases online. The best part about it is that it comes without unexpected bills, monthly contracts, or any other commitments since users only spend the amount that is loaded onto the card.

When choosing the Paysafecard payment method on the checkout page, users get redirected to the Paysafecard website, where they can either enter their 16-digit PIN or login to their eWallet using their ‘my paysafecard’ username and password.

Paysafecard is an excellent payment method that provides a high level of security and privacy. It’s a reliable, easy, and budget-friendly option, making it a popular choice among European online shoppers.

Blik

Blik stands out as a widely adopted system integrated into the mobile banking apps of most Polish banks. Over 90% of customers who bank with Polish financial institutions can harness the power of Blik through their mobile banking apps.

Blik is a secure, one-time payment method (non-recurring) that adds an extra layer of authentication to online transactions. To make an online payment with Blik, customers simply request a six-digit code from their banking app and input it into the payment collection form.

Following this, the bank sends a push notification to the customer’s mobile phone, requesting authorization for the payment via their banking app.

It’s worth noting that the Blik code has a short lifespan of 2 minutes, with customers having a 60-second window to grant authorization once the payment process begins. For safety reasons, if this window expires, a new Blik code must be requested.

Once the code is approved, the money transfer is made instantly.

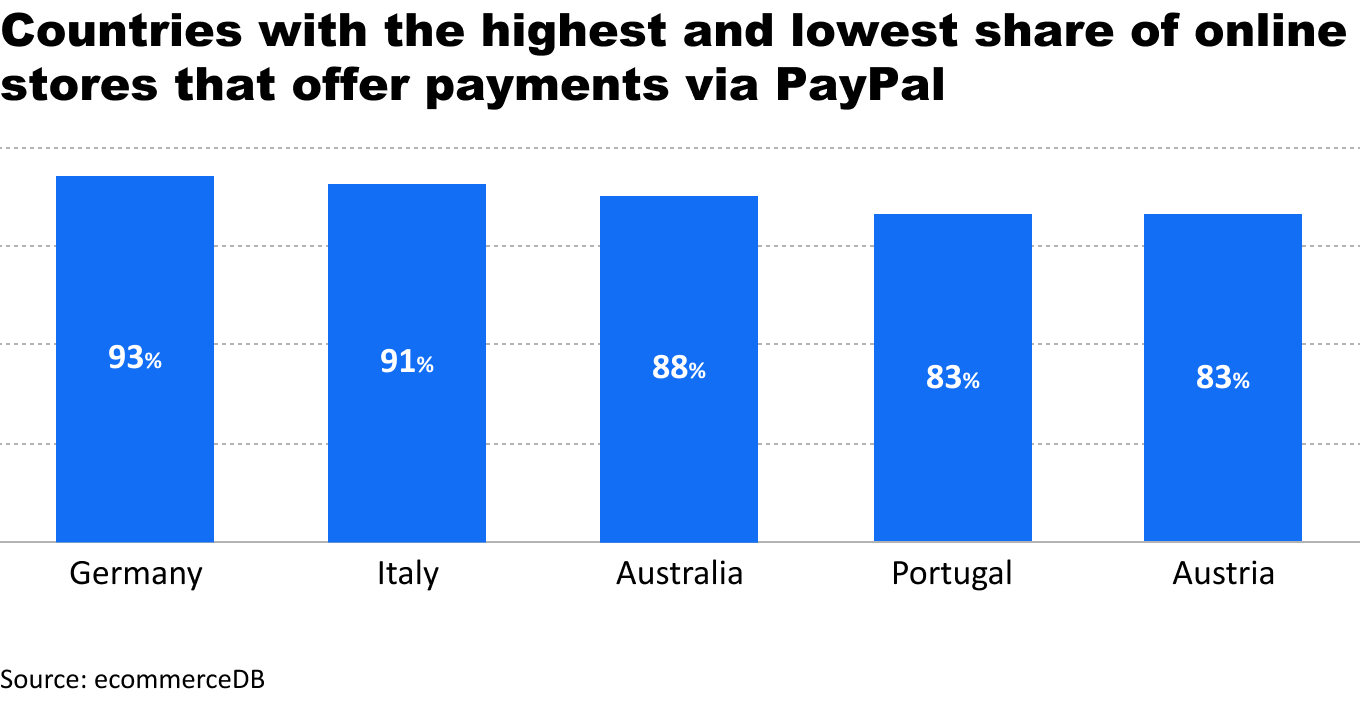

PayPal

According to ECDB, the dominance of PayPal as a payment choice among European online retailers is striking. Germany leads the pack, with an impressive 93% of its ecommerce stores embracing PayPal for transactions.

Italy closely follows with a 91% adoption rate. Portugal and Austria are within the top 5 countries globally (with Australia holding the third place), both boasting a substantial 83% utilization of PayPal by their ecommerce establishments.

PayPal is an eWallet. Users can fund their PayPal account or connect directly to their bank account or credit card.

When a payment is made, funds are transferred from the customer’s bank account to the seller’s PayPal account, with the electronic payment being funded by the buyer’s bank.

Apple Pay & Google Pay

Apple Pay and Google Pay are on the rise among European users, especially in Western European countries such as France, Germany, and the UK.

Since both payment methods are connected with credit or debit cards, they replace the card data with tokens to protect the original card numbers from being used during transactions.

Once the customer confirms the purchase, the payment has to be authenticated through biometric verification, PIN, pattern, password, or security code, depending on the device used and individual settings.

Sofort

Whereas PayPal operates as an electronic cash stash, Sofort streamlines the process, eliminating the necessity of transferring funds by directly tapping into established online banking systems.

Sofort is a top-tier payment option in Germany, drawing a significant chunk of users away from the conventional bank transfer route.

However, its popularity extends beyond Germany’s borders. It covers many European markets, including Austria, Belgium, the Czech Republic, France, Hungary, Italy, the Netherlands, the United Kingdom, Poland, Slovakia, Spain, and Switzerland.

What sets it apart is the extra layer of security that shields against fraudulent transactions. Before the payment is finalized, customers must complete a two-factor authentication process to give it the green light.

Since 2014, it’s been part of the Swedish Klarna Group.

Bizum

Bizum is a handy mobile app that allows its users to send and receive money instantly with just a few taps on their smartphones.

With its user-friendly interface, instant notifications, and high level of security, Bizum has quickly become a preferred payment option for many consumers and businesses alike.

Whether the user wants to split a bill with friends or pay for goods and services online, Bizum offers a fast and hassle-free way to make payments.

Since the requirement to use Bizum payments is to have a Spanish IBAN, Bizum services are only available for accounts opened in Spanish banks.

BNPL

BNPL stands for “Buy Now, Pay Later.” It’s a payment method that allows consumers to make a purchase and defer the payment over time, typically in a series of installments. BNPL services are often provided by third-party companies, which partner with retailers to offer this payment option to customers.

Due to their flexibility, BNPL services have gained popularity in various parts of the world, including the EU and the US.

It’s crucial to note that they are not a single payment method but rather a category of payment solutions offered by several companies. The most recognizable European BNPL providers include Swedish Klarna and Australian Afterpay (known outside of Europe as Clearpay).

Both services offer pay-in-four financing without any fees or interest. Opening an account or using their financing services with Klarna or Afterpay won’t incur customer charges.

However, it’s important to note that late payments may result in fees. Klarna imposes a late fee of $7, while Afterpay charges a minimum of $10 for tardy payments. A detailed comparison of the two leaders sheds more light and comes in handy when choosing the BNPL payment method.

The specific popularity of BNPL services can vary from one EU country to another, but overall, it has become a tempting alternative for online shoppers.

Europe Has Much More in Store

Though the examples above are just the tip of the iceberg, they depict the complexity of the European market and the challenges merchants must overcome to compete successfully.

Neither global card networks nor leading domestic payment methods can fully cover the topic. Depending on the country, you might find various payment solutions, such as invoice-based payments, virtual cards, e-money, banking apps, various systems enabling digital payments or mobile wallets.

The European Central Bank, in collaboration with the national central banks of the euro area, is exploring the potential introduction of a digital euro. This digital form of cash would serve as an alternative to traditional banknotes, accessible to everyone in the euro area.

To remain competitive, merchants must proactively track and adapt to the evolving payment needs of European markets.

Go Global with Local Payment Methods

While it’s no surprise that universal payment networks like Visa, Mastercard, and PayPal are widely popular in Europe, what’s interesting is how European customers prefer locally developed solutions that cater specifically to their needs.

Since the European payment landscape is remarkably diverse, customer preferences vary across the continent. Despite the widespread popularity of universal payment networks such as Visa, Mastercard, and PayPal, European shoppers tend to prefer locally developed solutions tailored to their unique requirements and needs.

That said, if merchants want to seriously plan for the international growth of their businesses, there’s no other way than to adapt their business model to local needs.

By offering payment options aligning with customer expectations, merchants can enhance their user experience, improve business conversion rates, and build brand trust.

Adding country-specific payment methods during checkout is a great competitive advantage that can unlock new market opportunities.

Keeping abreast of all the payment methods in Europe worthy of consideration may be challenging and time-consuming. Therefore, finding an experienced and reliable payment provider offering hassle-fee payment methods integration is critical. Why not try Shift4?

Take the first step and watch the video below to check out how our streamlined integration process empowers businesses to thrive!