Although the entire payment process takes seconds, various entities work behind the scenes to make this process work seamlessly for a frictionless customer experience.

Let’s dive deeper to better understand the roles and responsibilities of payment processors in the checkout process.

What Is a Payment Processor?

A payment processor — or a payment service provider — is a company or financial institution responsible for handling the logistics of a credit card transaction.

These entities get credit or debit card information and transfer it to the acquiring bank and the customer’s bank. When the customer’s account contains sufficient funds, the transaction gets approved.

Apart from transferring money, the payment processor is also responsible for checking whether the customer’s data is correct and keeping the process secure by analyzing fraud possibilities. In a way, the payment processor works as a mediator between the bank and the merchant.

A payment processor’s primary role is to verify with the customer’s card issuing bank or card association, determine whether the card details are correct, and perform anti-fraud measures to safeguard the transaction.

In addition to those responsibilities, payment processing companies can help businesses get their merchant accounts. And, if necessary, when a customer disputes a transaction, a payment processor is often the party that helps the merchant resolve it — a service that may come at an extra fee. Merchants should keep in mind that payment processors charge a fee for each transaction , an interchange fee, and also chargeback fees.

If a business prioritizes pricing when selecting a payment processor, it’s important to carefully review the terms of service to understand what is included with their costs. This could help to avoid costly unexpected fees in the future.

Payment Processing at a Glance

Before we delve deeper into the process itself, let’s explore the various parties involved in payment processing.

Apart from the obvious — a payment processor working behind the scenes — several other players are involved, including:

- Customer (who enters the card data)

- Merchant

- Payment processor

- Payment gateway (typically operated by a payment service provider)

- Customer’s bank or credit card company (the issuer)

- Merchant’s bank (the acquirer)

While the payment gateway is responsible for the transfer, the payment processor’s role is to authenticate and secure the transaction. As mentioned above, a payment processor verifies whether the payment data entered by the customer is correct.

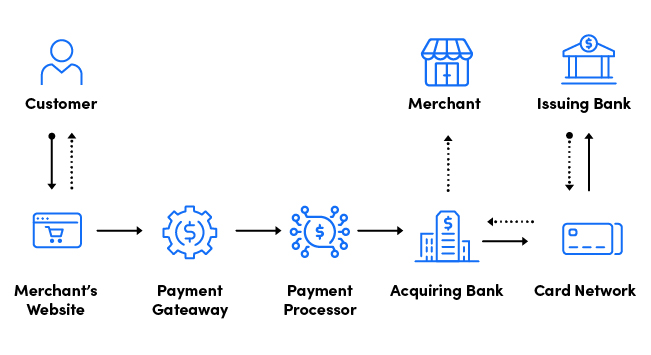

The entire operation usually takes up to just a few seconds and includes the following phases:

- The customer enters their card information on the merchant’s website, at a terminal in a store, or through any other payment method where card data is being used. The card data is submitted through the payment gateway.

- The payment gateway encrypts and sends the collected information to the payment processor.

- The payment processor sends the authorization request to the acquiring bank, which redirects the information to the card network (Visa, Mastercard, American Express, or others) for their approval.

- The transaction details are then forwarded to the issuing bank. The issuer thoroughly examines the customer’s account status, available balance, or credit limit and approves or declines the transaction.

- Once receiving the authorization response from the issuing bank, the card network returns through the acquiring bank to the payment processor with the information indicating whether or not the payment request is approved.

- If approved, the merchant finalizes the transaction initiated by the customer. If the transaction is declined, the merchant can ask the customer to use an alternative payment method.

- For approved transactions, the payment processor informs the issuing bank (the one that issued the customer’s card) that the funds can be sent to the acquiring (merchant’s) bank as soon as the transaction is complete.

- Depending on the payment provider, the account type, and the payment method chosen, the merchant receives funds immediately or within a few business days.

Sometimes a transaction is declined. In this scenario, the merchant receives a decline code so they know the reason for the cancellation.

It’s important to know that not every transaction decline results from a lack of funds or criminal fraud. Some declines may result from system errors, the card itself, or communication errors between banks and processors.

How to Start Working With a Payment Processor

Before merchants choose the payment processor they want to work with, they must consider several aspects to ensure it meets their business needs.

We suggest starting with the following:

- Accepted Business Models: It’s not surprising that this is first on the list. It’s highly recommended that merchants ensure that the credit card processor they choose offers solutions for the industries their company operates in before they apply for a merchant account. The same goes for countries and payment cards.

- Technology: To have full control over the setup and payment process, merchants (especially online merchants) should search for a payment processor offering application programming interfaces (APIs). They must ensure that the payment processor provides the latest technology, know-how, and procedures for fast onboarding and painless payment flow without downtime or surprises.

Merchants interested in multiple accounts should check if this option is available. The same applies to the possibility of implementing various scenarios that align with their business needs, which can be critical — especially for complex business models.

It’s advisable to check if the online payment form feature offered by the payment processor is fully customizable and if the payment processor provides all the features necessary to offer customers a flawless experience.

From the technical point of view, it is possible to work with different entities and benefit from a merchant account, a payment gateway, and payment processing provided separately. However — for optimization purposes — it’s better to work with a single provider that offers an all-in-one solution like Shift4. As a result, many payment processing complexities can be avoided. - Security: It’s key to find a payment processing provider that adheres to strict security rules and provides a set of anti-fraud tools to protect a merchant’s business. A payment processor that offers a multi-layered approach to security will help reduce suspicious activity and deliver a decent chargeback prevention system.

- Expertise: Since merchants entrust their money to the payment provider, it is highly recommended to do some research before signing a final agreement. Merchants must be sure that the expertise and know-how they pay for are exactly what they need and expect.

- Transparent Pricing: Without a doubt, merchants have the right to understand pricing before they sign a contract with a payment processor. They must be sure that the fee structure is clear and that there aren’t any hidden or extra fees.

- Customer Support: Responsive customer support that will help merchants quickly resolve payment issues is a necessity. After all, it’s about the customers’ money and the merchants’ business reputation. Merchants should select a payment process that will address every problem quickly and professionally.

Secure Payment Processing is Key to Business Growth

A reliable payment provider can make merchants’ lives easier as it takes on the responsibilities of securing and carrying out transactions, thus helping businesses grow.

For this reason, finding a proper business partner should be preceded by an in-depth topic analysis — regardless of whether the merchant applies for a payment processor through a bank or a provider’s website.

Without question, it’s better to spend twice as much time checking every aspect and analyzing the payment processor contract thoroughly to ensure that the right choice was made.